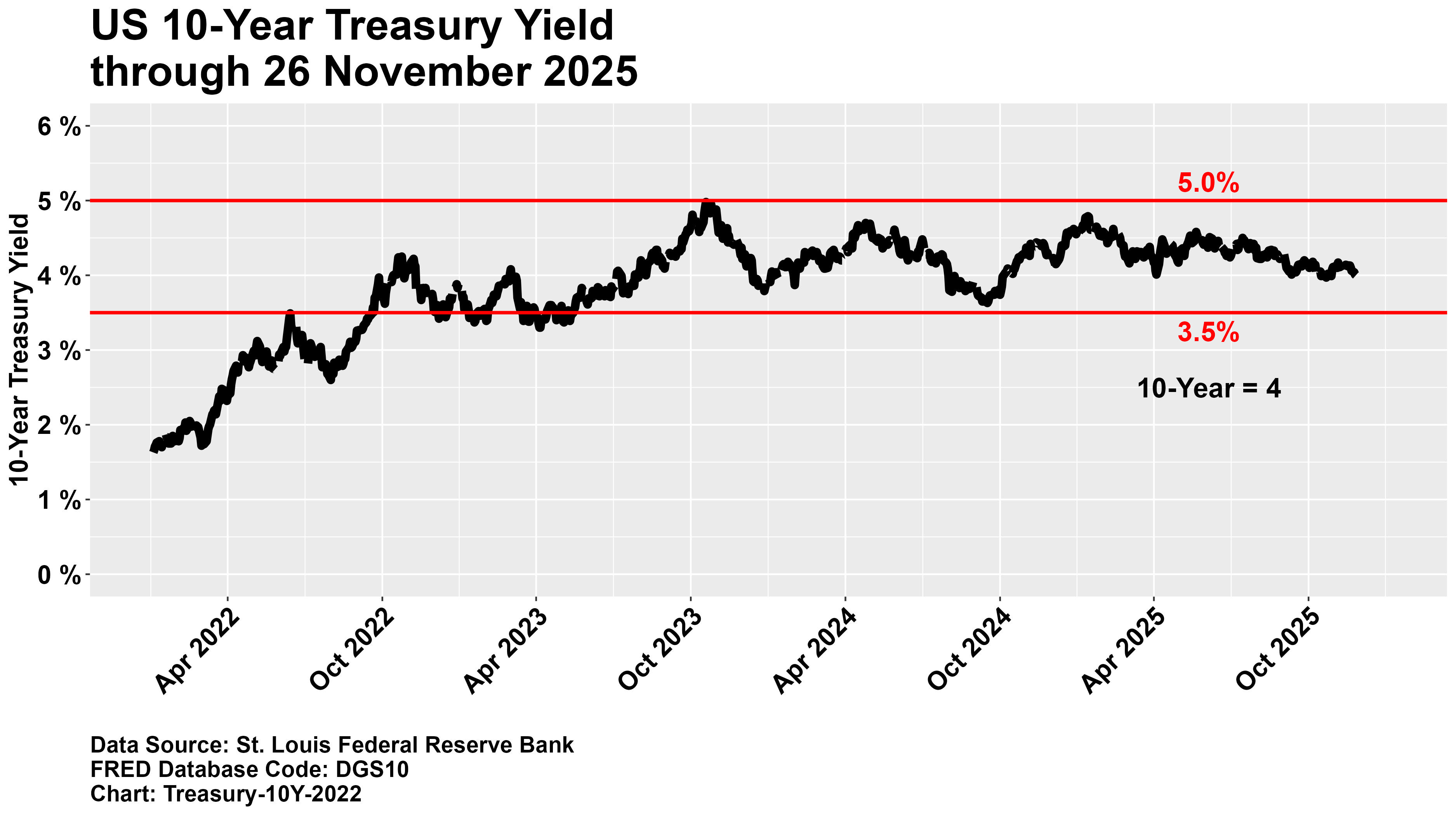

Confidence and Rate Probability Distributions

When new information causes market participants to revise their expectations, confidence is also revised. As the forecasting time horizon lengthens, typically confidence in one's forecasts diminishes. Moreoever, there is the possibility that probability distributions may take on highly skewed shapes or even have two modes, reflecting two different senarios that are competing for the attention of market participants. Our probability analysis is designed to be independent of any pre-defined distribution. Our analysis starts with the presumption of a bell-shaped curve (i.e., something similar to a normal distribution), but we allow information from a variety of metrics derived from market activity to suggest that the hypothetical probability distribution might take on a very different shape, with important implications for risk management.

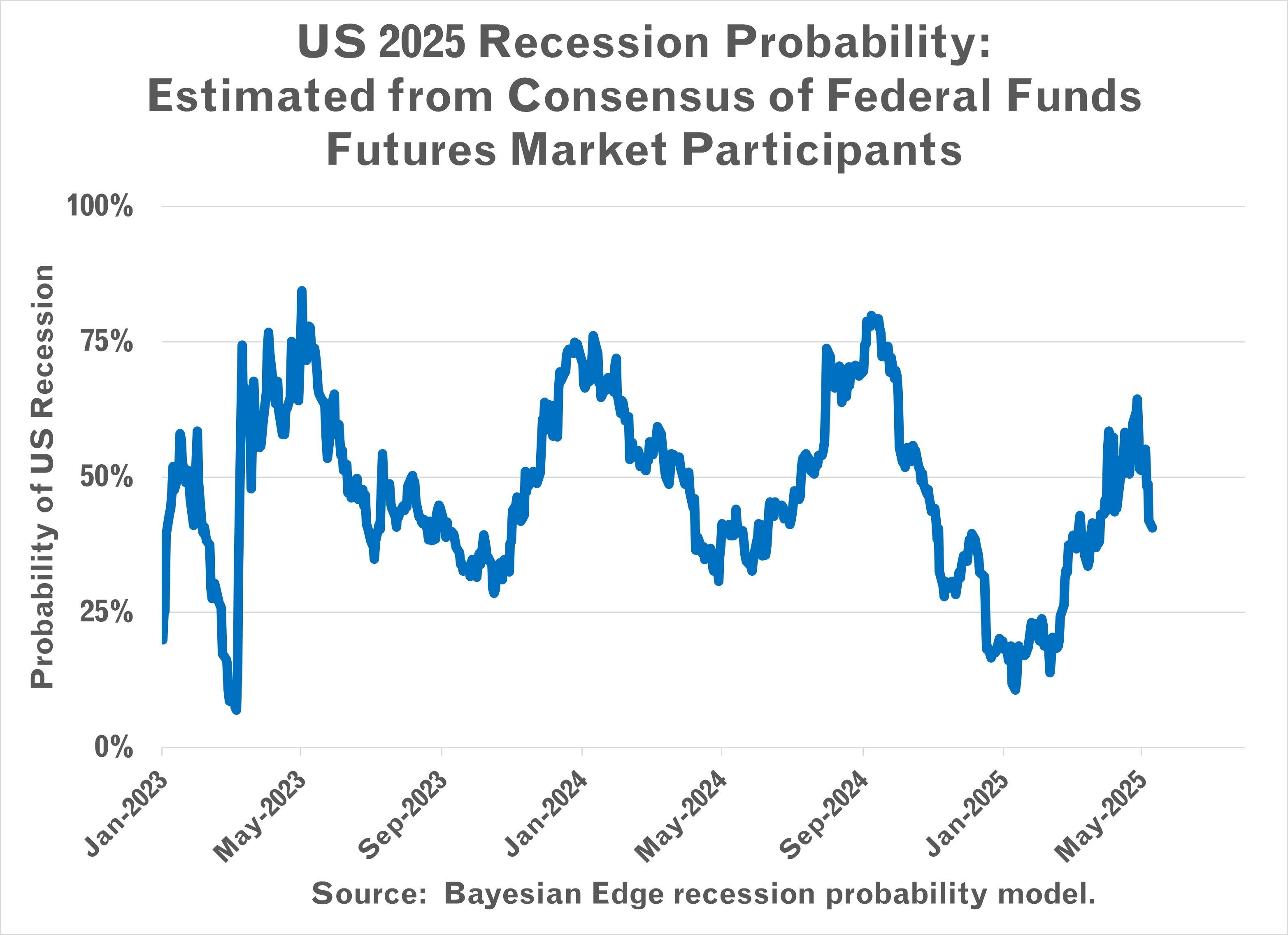

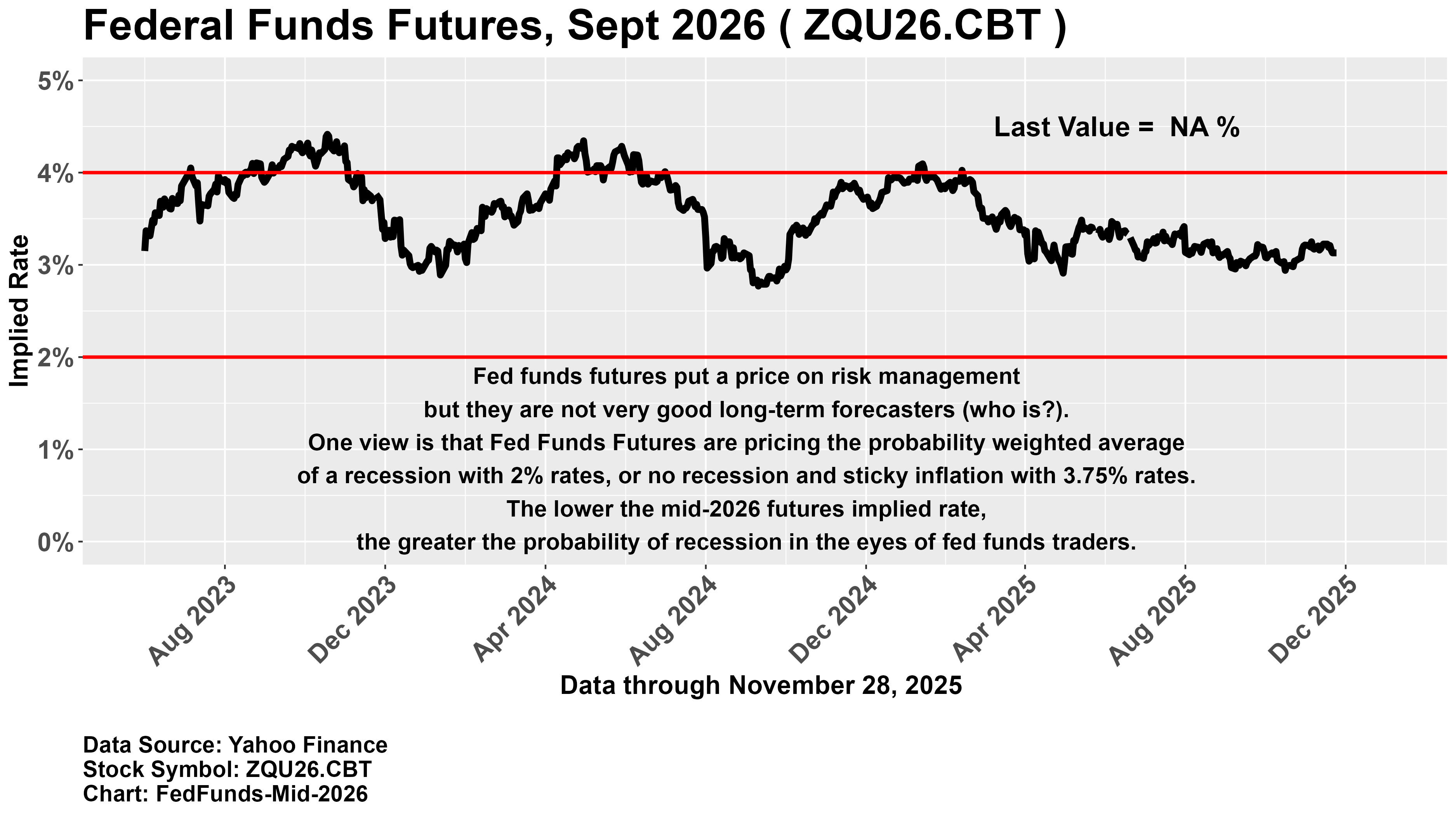

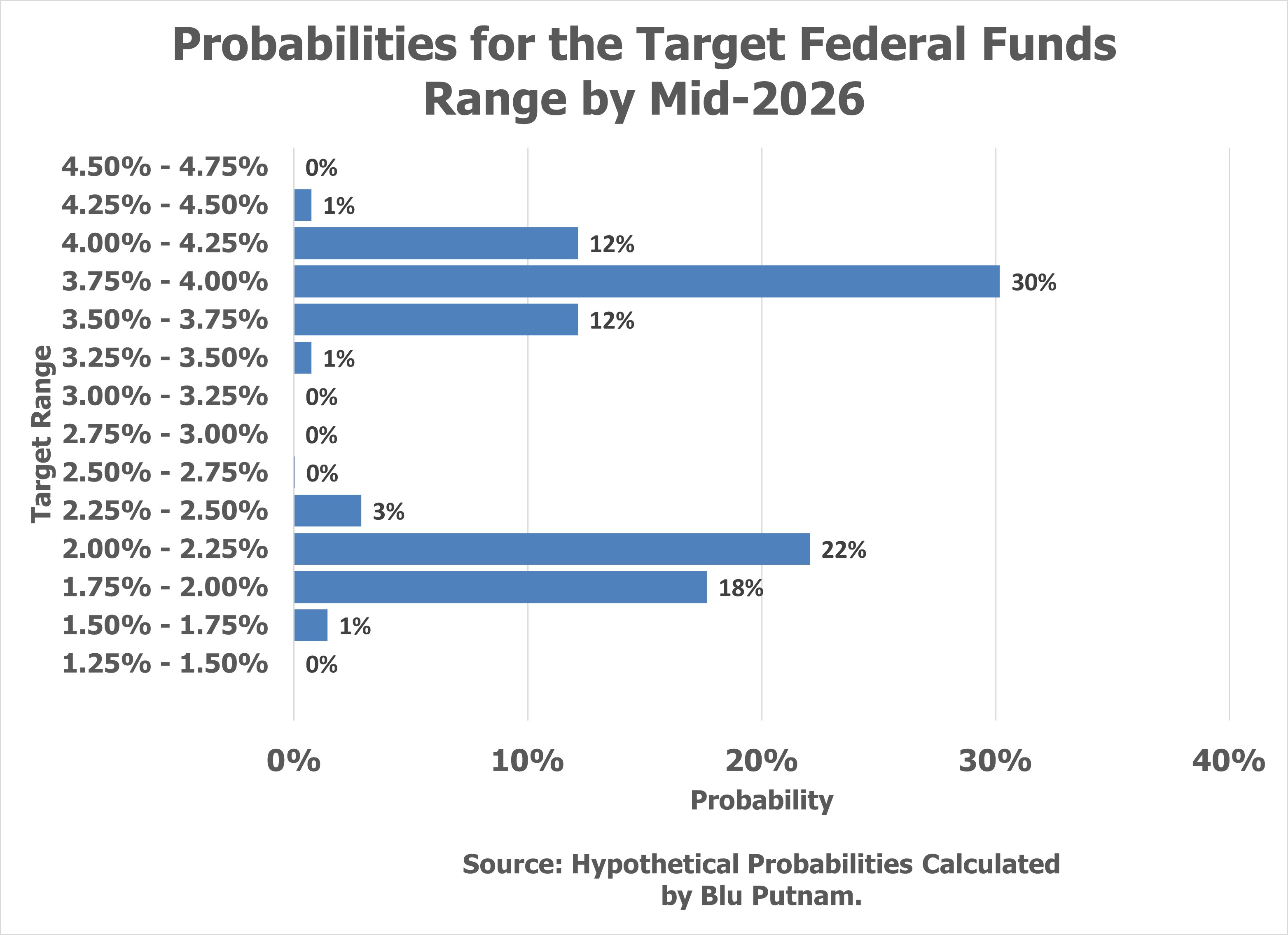

Hypothetical Recession Probability Derived from Federal Funds Futures

Might it be possible to calculate what market participants think about US recession or no-recession probabilities from federal funds futures prices? Yes, although with a heavy burden of heroic assumptions.

Warning: the consensus expectations of market participants are likely to be wrong and they move around with every new piece of information. So, be careful how one interprets this hypothetical analysis.

Now for the assumptions. We are assuming the federal funds futures prices should NOT be interpreted as the market expectations of the rate in the future, as is commonly done. We believe that there are two dominant scenarios, and the futures market is pricing the probability-weighted average of the two. Scenario #1 assumes no recession, inflation is sticky above the Fed’s 2% target, and the Fed is only willing eventually to lower rates to the 4.00% - 4.25% target range. Scenario #2 assumes a recession, inflation drops below 2%, and the Fed lowers rates to around 2% or slightly lower to stimulate the economy.

Only one of these scenarios (or maybe even some other scenario) will prevail, which is why we do not recommend interpreting the implied interest rate from federal funds futures as a point forecast when market participants are debating multiple scenarios. Futures markets price the cost of hedging directional risk, which depends on the views of hedgers and speculators and how they assign probabilities to different scenarios.